[Riassuntu] I prezzi di cuttuni domestici o continueranu à esse bassu scossa. A stagione di punta tradiziunale di u mercatu tessili s'avvicina, ma a dumanda attuale ùn hè ancu emersa, a probabilità di l'imprese tessili per apre hè sempre in calata, è u prezzu di u filatu di cuttuni cuntinueghja à falà. Attualmente, a crescita di u cuttuni novu domesticu hè bonu, l'aumentu di a produzzione hè prevista per esse senza cambià è u tempu di lista pò esse prima di l'annu passatu. À u listessu tempu, a quota di l'impurtanza di l'impurtazione di cuttuni sliding serà emessa prestu, è a pressione discendente nantu à i prezzi di u cuttuni domesticu ùn diminuirà micca.

I. A rivista di u prezzu di sta settimana

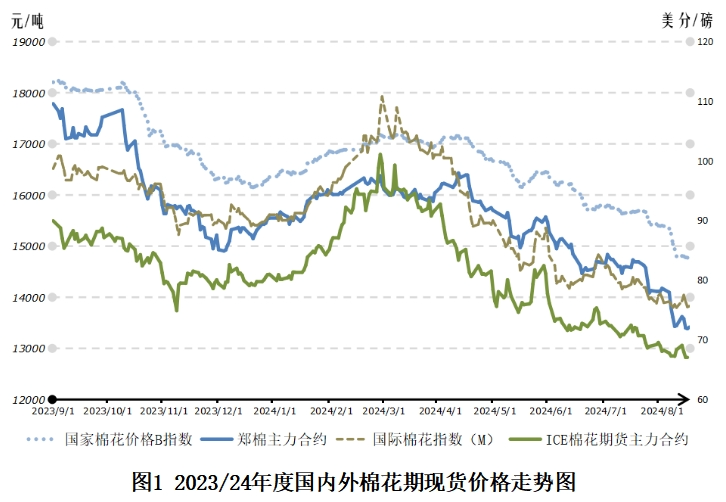

Da u 12 à u 16 d'aostu, u prezzu mediu di a liquidazione di u cuntrattu principale di u futuru di u cuttuni Zhengzhou era 13.480 yuan/ton, 192 yuan/ton da a settimana precedente, 1,4%; L'indice naziunale di u prezzu B di u cuttuni, chì rapprisenta u prezzu di u mercatu di u filu di qualità standard in u cuntinente, hà una media di 14 784 yuan/ton, in cala di 290 yuan/ton da a settimana precedente, o 1,9%. New York cotton futures cuntratti principali stabilimentu prezzu mediu di 67,7 centesimi / libbra, up 0,03 centesimi / libbra da a settimana precedente, basicamente flat; U prezzu mediu di l'indici internaziunale di cuttuni (M) chì rapprisenta u prezzu mediu sbarcatu di u cuttuni impurtatu in u portu principale di a Cina era di 76,32 centesimi / libbra, più di 0,5 centesimi / libbra da a settimana precedente, è u costu d'importazione di RMB 13,211 yuan / ton ( calculatu da a tarifa 1%, escludendu a miscellanea è u trasportu di Hong Kong), in crescita di 88 yuan/ton da a settimana precedente, un aumentu di 0,7%. U prezzu di u cuttuni domesticu hè 1573 yuan/ton più altu ch'è u prezzu internaziunale di cuttuni, chì hè 378 yuan/ton più strettu di a settimana precedente. U prezzu mediu di u filatu di cuttuni puri C32S generale pettine domesticu hè di 21.758 yuan/ton, in calata di 147 yuan/ton da a settimana precedente. U prezzu di u filatu cunvinziunali hè 22222 yuan / ton, chì hè u listessu cum'è a settimana precedente. U prezzu di a fibra di poliester hè 7488 yuan/ton, in calata di 64 yuan/ton da a settimana precedente.

Siconda, a prospettiva di u mercatu vicinu

(1) Mercatu internaziunale

Fattori favurevuli sò apparsu, i prezzi di cuttuni o stabilizzaranu. U rapportu di l'offerta è di a dumanda di u Dipartimentu di l'Agricultura di i Stati Uniti d'aostu prevede una pruduzzione di cuttuni di i Stati Uniti di 3,29 milioni di tunnellate in 2024/25, una diminuzione di 410 000 tunnellate da u mese precedente, principalmente per via di a recente siccità aggravata in a regione produttrice di cuttuni di i Stati Uniti. U USDA Drought Monitor informa chì circa u 22 per centu di e zone di pruduzzioni di cuttuni sò affettati da a siccità da sta settimana, da u 13 per centu a settimana prima. Sicondu statistiche di u Ministeru di l'Agricultura Indianu, à l'8 d'Aostu 2024/25, a zona di piantazione di cuttuni in India era di 166 milioni di mu, in diminuzione di l'8,9% annu à l'annu, è a pruduzzione hè prevista per diminuite di 370 000 tunnellate annu. annu. Intantu, i dati di u Dipartimentu di u Cummerciu di i Stati Uniti anu dimustratu chì u cunsumu di u cumerciu di i Stati Uniti hà aumentatu 1 per centu in lugliu da u mese precedente, u più altu livellu da u ferraghju 2023, facendu u mercatu menu preoccupatu per a recessione di i Stati Uniti, chì furnisce u sustegnu per u sentimentu migliuratu in u mercatu di e materie prime. Sicondu u rapportu di a Cummissione Commodity Futures Trading di i Stati Uniti, da u 6 d'aostu, i futuri di cuttuni ICE cummirciali (pruduttori, cummircianti, prucessori) nette pusizioni longu 1156, per a prima volta da 2019 à turnà net, significatu chì i fondi di l'industria crede chì u cuttuni internaziunale. i prezzi o sò intruti in a gamma di valutazione bassa. Cumminatu cù i fatturi sopra, i prezzi internaziunali di u cuttuni sò previsti per stabilizzà.

(2) U mercatu domesticu

A dumanda downstream ùn hà micca vistu u principiu, i prezzi di u cuttuni cuntinuavanu à fluttuà à un livellu bassu. Sicondu l'Uffiziu Naziunale di Statistiche, a vendita di vendita di vestiti, scarpi, cappelli è prudutti tessili in Cina in lugliu era di 93,6 miliardi di yuan, in calata di 5,2% annu annu; I dati doganali anu dimustratu chì l'esportazioni di tessili è vestiti di a Cina in lugliu eranu 26,8 miliardi di dollari americani, in calata di 0,5% annu annu. Dapoi l'aostu, u mercatu domesticu hà aspittatu à a prossima stagione di dumanda tradiziunale di "oru nove d'argentu dieci", ma l'ordine ùn anu ancu mostratu segni di migliuramentu. Sicondu l'indagine di u sistema di surviglianza di u mercatu naziunale di cuttuni, à principiu di aostu era un sondaghju di mostra di l'imprese tessili per apre a probabilità di 73,6%, falà 0,8 punti percentuali da u mese precedente, solu variità di filati grossi individuali mostranu certi signali di riscaldamentu, u terminal. mercatu wake-and-see atmosfera hè sempre pisanti, sta settimana i prezzi di filati di cuttuni domestici cuntinueghjanu à calà. Attualmente, a crescita di u cuttuni hè megliu, hè aspittatu chì u tempu di lista di cuttuni pò esse prima di l'annu passatu, è a quota di l'impurtanza di l'impurtazione di u cuttuni hè per esse emessa, chì pò esse più pressione nantu à i prezzi di u cuttuni domesticu, è a pussibilità di cuntinuà scossa bassa hè più grande.

Tempu di post: Aug-19-2024